Bought some 6330 Toyo Engineering

A boring business that is hard to stop thinking about

In my view, multiple thematic drivers are converging upon this stock, such that this cheap stock will naturally rerate to 2,000 yen per share (1,043 yen per share on July 16, 2025) or be taken out by parent Mitsui & Co at a similarly compelling premium.

Business

Toyo Engineering Corporation (6330) is a plant engineering company that handles the design, procurement, and construction of manufacturing facilities for fertilizers, petrochemicals, oil, and gas. The company was established in 1961 as a spin-off from the engineering department of 4183 Mitsui Chemicals, a chemical manufacturer specializing in fertilizers such as ammonia and urea.

Metrics: At share price of 1,043 yen per share, market cap of 40.2 bil yen / net cash of 25 bil yen / 8.00x PER / 0.89x PBR / 2.40% yield.

Driver #1: Small-cap net-cash

No doubt inspired by legendary HF manager Tatsuro Kiyohara, I love Japanese small-cap net-cash stocks. The opportunities are too often overlooked in that space. It is a blue ocean in investing business.

With equity market cap at 40 bil yen and net cash of 25 bil yen, their business is valued at 15 bil. Therefore, on a cash-neutral basis, the company is worth 7.5x LTM PER (2.0 bil yen of after-tax earning), and 3x NTM PER (5.0 bil yen of after-tax earning). The company expects to earn 10.0 bil yen after-tax in 2030.

These metrics alone might make someone bullish. But there’s more.

Driver #2: No tariff war exposure

The company makes clear that their operations are little affected by the current tariff war, because there are few projects within the U.S. territory and they procure no equipment from there either.

In fact, Toyo is beautifully diversified in terms of geography and end-client segments:

Driver #3: Shift to recurring revenue model, with positive outlook

Toyo’s traditional business consists of what they call an “EPC” business, meaning they do plant engineering, (raw material) procurement, and construction. But they are aggressively growing their recurring rev business model, such as energy-efficiency consulting, greenhouse gas reduction service, fuel ammonia feasibility study service and urea-related licensing.

That would give them less volatility in earnings, and a higher profit margin. They already achieved 2030 target of “50% of company-wide gross profit to come from non-EPC business” in fiscal 2023. Now they are in the phase of growing both segments in absolute value terms.

The management thinks they can double their net income in the next 5 years.

Driver #4: Rare earth play

Toyo is a hot geopolitical / national security play. The company stands to benefit from the Japanese Government initiatives to increase its rare earth self-sufficiency rate.

Toyo Engineering has been participating since 2019 in the development of technology for a rare earth mud recovery system located in the exclusive economic zone (EEZ) off Minamitori Island. This project, led by the Japan Agency for Marine-Earth Science and Technology (JAMSTEC) under the Cabinet Office’s Strategic Innovation Promotion Program (SIP), aims to establish the world’s first technology for recovering rare earths from a depth of 6,000 meters.

Toyo is responsible for optimizing a subsea production system equipped with stirring blades, pumps, valves, monitoring sensors, and other components. Its efforts have been highly regarded, with the project being featured in the scientific journal “Nature”.

Source: https://www.nature.com/articles/d42473-020-00524-y

Driver #5: Dual-listing

8031 Mitsui & Co., of which the Berkshire Hathaway group famously owns 10%, owns 23% of Toyo.

Several Board members of Toyo, including some of the predecessor CEOs, are originally from Mitsui & Co or other Mitsui zaibatsu group. So, even with 23% ownership, this should qualify as a “parent-child” dual listing situation, which the Tokyo Stock Exchange is crusading against.

Mitsui & Co has several incentives to make this dual-listing problem go away: to appease the TSE, to prove their adept capital allocation skills in front of Berkshire, and - most importantly - to tightly control the subsidiary operations in their strategically core sector.

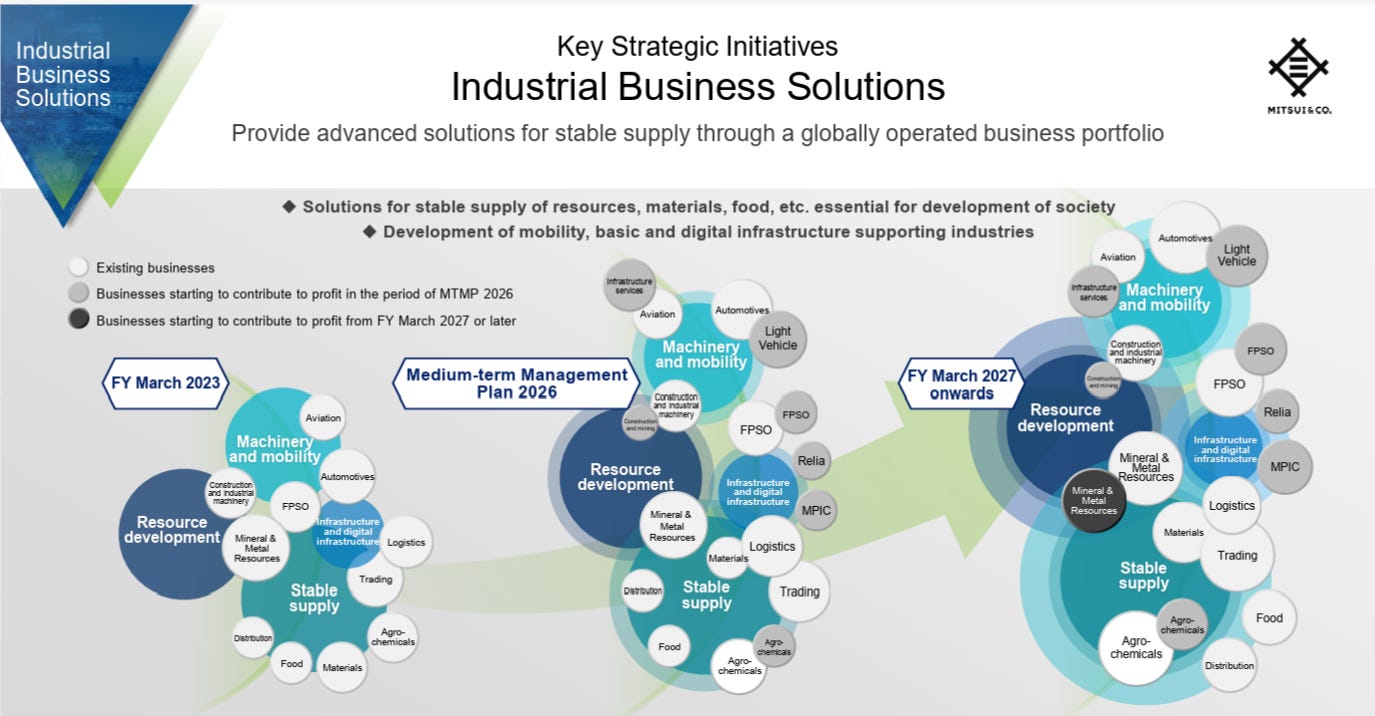

And what does Mitsui & Co’s Mid-term Management Plan 2026 say about one of their key strategic initiative is? Development of natural resources to support industrial infrastructure for a futuristic mobile and digital society.

To repeat, this is not Toyo’s mid-term plan. It is Mitsui’s.

Source: https://www.mitsui.com/jp/en/company/outline/management/index.html

Driver #6: Technical chart

Over the past few weeks, Japan’s rare earth-related stocks, including Toyo Engineering, have seen notable gains. This surge is driven by heightened awareness of the importance of rare earths, triggered by China's export restrictions, combined with reports of rare earth test drilling off Minamitori Island.

I am no technical analyst, but I recognize what I am seeing here.

End Note

In sum, Toyo Engineering is:

(i) a small-cap net-cash stock trading at 3x NTM PER with a growth outlook

(ii) not exposed to tariff wars

(iii) successfully shifting to a recurring rev model with its decades of IP and other soft assets, potentially helping with the multiple expansion

(iv) a national security / rare earth play when “China vs. Taiwan” may dominate our headlines any time now, and

(v) a dual listing play

– all in one, in a bullish technical landscape.

Add to this a view that the rising JGB yield is arguably bullish for companies with net cash and low multiple (i.e., theoretically the cash earns market returns, while some capital in market may gravitate toward the low multiple stocks in a flight to safety).

Toyo's plant construction business might sound boring, but when viewed through the lens of a trading thesis, it's anything but mundane.

Disclaimer: The content on this blog is for informational purposes only and does not constitute investment advice. No information provided guarantees factual accuracy or predicts the future performance of any stock or asset. Readers should conduct their own research and consult a qualified financial advisor before making investment decisions. The author is not liable for any losses or damages arising from the use of this content.